The number the bank shows you vs the number that matters

Banks present the monthly EMI because it is the smallest, most comfortable number in the loan equation. It fits in your monthly budget calculation. It sounds manageable. What the EMI figure alone does not tell you is the total interest cost over the full tenure — which on a typical home loan is often larger than the loan amount itself.

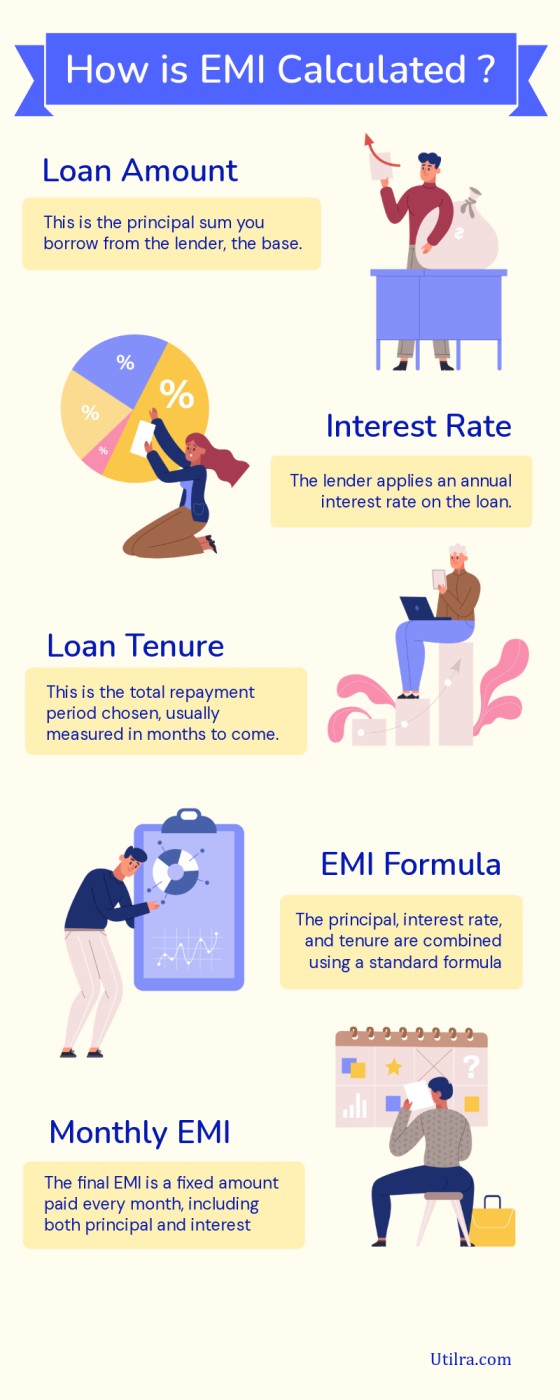

Three factors determine your EMI entirely: the loan amount, the interest rate, and the tenure. Change any one of them and every other number changes. The relationship between these three variables is not linear and not intuitive — which is exactly why a home loan emi calculator is the right tool before any conversation with a lender, not after.

Home loan EMI calculator — three borrowers, same ₹50 lakh loan

Rohan, Preethi, and Suresh each borrow ₹50 lakh from the same bank at 8.5% interest. They choose different tenures. Here is what that single decision produces in real numbers.

Rohan chooses 10 years. His EMI is ₹61,944 per month. At the end of 10 years he has paid ₹74,33,280 in total — ₹24,33,280 in interest on a ₹50 lakh loan. His monthly commitment is high but his total outflow is the lowest of the three.

Preethi chooses 20 years. Her EMI is ₹43,391 per month — ₹18,553 less than Rohan every month. That saving feels significant. But at the end of 20 years she has paid ₹1,04,13,840 in total — ₹54,13,840 in interest. She paid more in interest than the original loan amount, and nearly ₹30 lakh more than Rohan across the full tenure.

Suresh chooses 30 years. His EMI drops to ₹38,446 — the lowest of the three, just ₹23,445 less than Rohan per month. His total outflow over 30 years: ₹1,38,40,560. He pays ₹88,40,560 in interest — nearly 1.77x the original loan. He pays ₹64 lakh more than Rohan for the same ₹50 lakh borrowed.

The monthly difference between a 10-year and 30-year tenure is ₹23,445. The total difference over the life of the loan is ₹64 lakh. That is the trade-off that a home loan emi calculator makes visible before you commit.

How a 1% rate difference compounds over time

Tenure is the first variable most people think about. Interest rate is the second — and it compounds just as dramatically.

On the same ₹50 lakh loan for 20 years, here is what different interest rates produce:

| Interest rate | Monthly EMI | Total interest paid | Total outflow |

|---|---|---|---|

| 7.5% | ₹40,280 | ₹46,67,200 | ₹96,67,200 |

| 8.5% | ₹43,391 | ₹54,13,840 | ₹1,04,13,840 |

| 9.5% | ₹46,607 | ₹61,85,680 | ₹1,11,85,680 |

| 10.5% | ₹49,919 | ₹69,80,560 | ₹1,19,80,560 |

The difference between a 7.5% loan and a 9.5% loan is ₹6,327 per month and ₹15,18,480 in total interest over 20 years. Two percentage points on the interest rate costs more than ₹15 lakh on a ₹50 lakh loan. This is why comparing lenders and negotiating your rate — even by 0.25% — is worth the time before signing.

You can run these comparisons instantly using Utilra’s free home loan EMI calculator — enter your loan amount, the rate you’ve been quoted, and your preferred tenure to see the full picture in seconds.

The prepayment strategy — what the home loan emi calculator doesn’t show

Preethi took the 20-year loan at ₹43,391 per month — the middle option. But she used a strategy that most borrowers overlook.

Every year, when her annual bonus arrived, she made one additional EMI payment directly against the principal. That is approximately ₹43,391 extra per year on top of her regular payments. According to RBI guidelines, banks cannot charge prepayment penalties on floating rate home loans. The extra payment goes entirely to reducing the outstanding principal, which reduces the interest calculated on it every month thereafter.

The result: one extra EMI per year on a 20-year floating rate loan reduces the effective tenure by approximately 4–5 years and saves several lakh in interest — without the pressure of committing to a higher monthly EMI from day one.

This is the middle path that makes the most financial sense for most salaried borrowers. Take the longer tenure for EMI comfort. Prepay systematically whenever extra income arrives. The home loan emi calculator shows you the original schedule; the prepayment effect is what changes the outcome.

Fixed rate vs floating rate — what changes in 2026

Most home loans in India today are linked to an external benchmark — typically the RBI repo rate — which means your interest rate floats with monetary policy decisions. When the RBI cuts rates, your EMI reduces. When it raises rates, your EMI increases. For 2026, with the RBI in a cautious easing cycle, floating rate borrowers have generally benefited from modest rate reductions over the past year.

Fixed rate home loans lock your rate for the entire tenure — or sometimes for a fixed initial period of 2–3 years before converting to floating. Fixed rates are typically higher than prevailing floating rates because the lender absorbs the rate movement risk. In a falling rate environment, fixed rate borrowers do not benefit from reductions.

The practical recommendation for most new borrowers in 2026: floating rate loans at a competitive margin over the repo rate, with a prepayment plan to reduce tenure when income allows.

What the 40% rule actually means

A widely used guideline in personal finance is to keep your total EMI commitments — home loan, car loan, personal loans — within 40–50% of your net monthly take-home income. This is not a bank rule; it is a personal financial health guideline.

At ₹43,391 EMI on a ₹50 lakh loan, the 40% rule suggests a net monthly income of approximately ₹1,08,000 or above. Banks will often approve loans where the EMI is 50–55% of income — they are optimising for loan disbursement, not for your financial comfort. Running a home loan emi calculator against your actual take-home salary, not your gross salary, gives you the honest number.

Keep enough margin for life events — a job change, a medical expense, a period of reduced income. The most stressful loans are the ones that were affordable until something changed.

Home loan EMI calculator — what to calculate before visiting any bank

Before your first bank meeting, know four numbers: the EMI at your target loan amount and expected rate for your preferred tenure; the total interest you will pay at that tenure; the EMI at one tenure shorter (15 years if you were planning 20); and the total interest saving that shorter tenure produces.

Walking in with these numbers changes the conversation. You are no longer reacting to what the bank presents — you are evaluating it against a baseline you already understand. A 0.25% lower rate becomes a specific rupee saving you can calculate. A longer tenure offer becomes a specific extra interest cost you can reject.

If you are also deciding how to invest the difference between a higher EMI and a lower one, the PPF vs FD comparison and FD calculator on Utilra help you run those scenarios alongside your EMI numbers.

All EMI figures in this article are illustrative estimates calculated at fixed rates for educational purposes only. Actual EMI depends on your specific rate, lender terms, and processing charges. Interest rates change frequently. Verify current rates with your lender and consult a qualified financial advisor before any borrowing decision.